Title here

Summary here

April 28, 202410 minutes

Earnings summary of my holdings in Q1 2024.

I wanted to start this series of posts primarily for two reasons:

Unfortunately, I haven’t been tracking some basic portfolio statistics, so this blog post gives me an opportunity to start doing so:

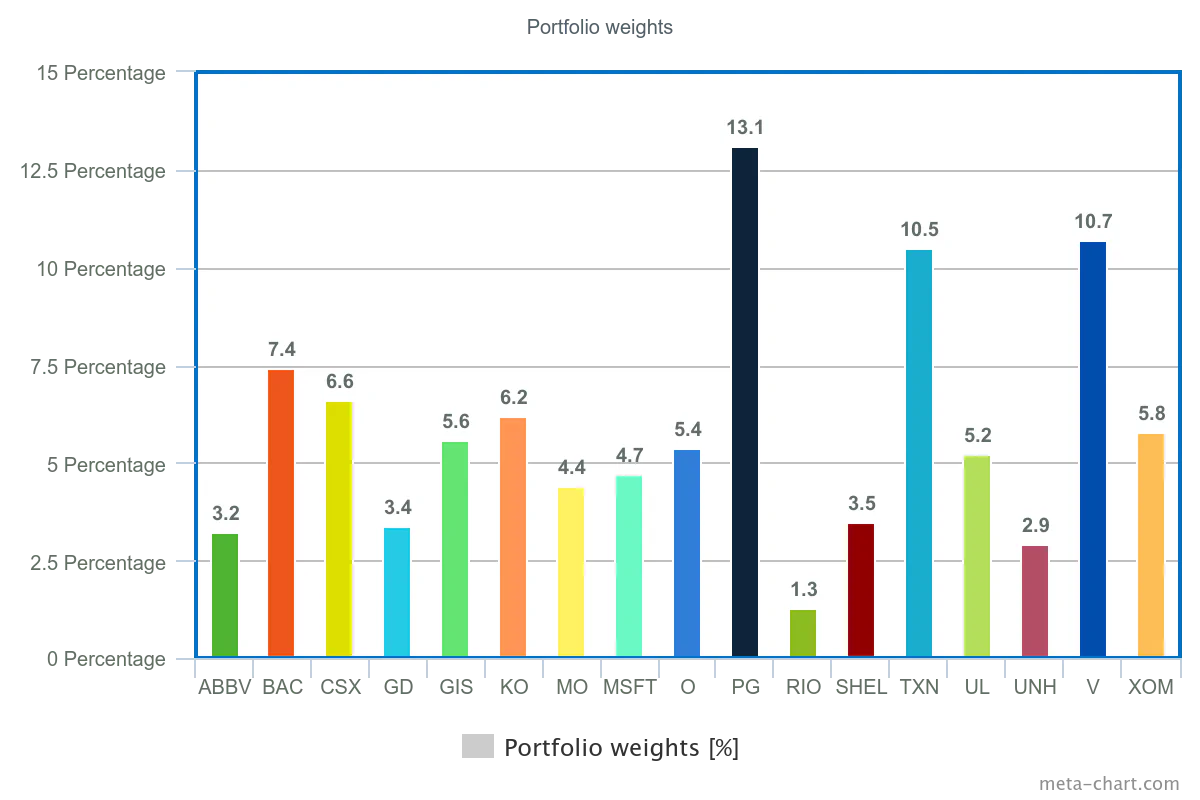

Picture below shows my current holdings as of end of first quarter 2024.

The newest additions to my portfolio, along with General Dynamics, include UnitedHealth Group. With this acquisition, I aimed to expand my exposure to the healthcare sector.

It wasn’t the best quarter ever, but stable revenue increases are always positive. The company returned just over $4.8 billion (+35% y/y) to shareholders over the quarter. FCF was $401 million, which wasn’t enough to cover the shareholder returns. However, this was affected by $3 billion in cyberattack response actions, including funding acceleration to care providers, and was further impacted by the timing of public sector cash receipts. Although UnitedHealth Group secured significant contracts in Texas, Virginia, and Michigan, it lost customers both y/y (-1.415 million) and q/q (-1.275 million).

UnitedHealth Group estimates direct response costs of $0.85 to $0.95 per share for the full year 2024. The company maintained its adjusted net earnings outlook of $27.50 to $28.00 per share. This adjusted earnings per share outlook excludes the impacts of the direct response costs and the Brazil sale while including the estimated $0.30 to $0.40 per share of business disruption impacts for the affected Change Healthcare services.

It was quite a quarter for UnitedHealth. Cyberattack response measures and unfavorable impacts from their Brazil business sale ate into profits. Although some IT systems are not yet restored, I believe they will manage to resolve it by the end of Q2. My target portfolio weight for UNH remains unchanged at 7.5%.

As always, Microsoft delivered. Revenues were up 17% y/y, and net income increased to 20% y/y. What is most impressive, though, is Cloud revenue up 23% y/y. After searching for the phrase ‘decreased’ in the press release, I only found one entry: Devices revenue decreased 17%. The company returned $8.4 billion to shareholders during the quarter.

I can’t say much more. The company is growing, investing heavily in Cloud and AI. My target portfolio weight for Microsoft remains unchanged at 7.5%.

I like the earnings releases from General Dynamics. They are short and informative. Revenue, operating earnings, and operating margin were up y/y (+8.6%, +10.4%, up 20 basis points). Earnings missed the analyst estimates by $0.07.

The recent FAA certification of the Gulfstream G700 has enabled the company to begin customer deliveries. The overall backlog for products was up 4.4% y/y. Some significant orders in the quarter include:

During the quarter, the company invested $159 million in capital expenditures, paid $361 million in dividends, and used $105 million to repurchase more than 390,000 shares, ending the quarter with $1 billion in cash and equivalents.

It was a good quarter for General Dynamics, though the market didn’t like it much. My target portfolio weight for the company remains unchanged at 5%.

This is one of my favorites in my portfolio. I love US railroads for their huge moat. I even did some railroad comparisons some time ago, which you can check here! My problem with them, though, is they usually spend more money on shareholder returns than they should. This wasn’t the case this quarter. But let’s start with some basics.

Revenue declined 1% y/y, operating income fell 8% y/y as lower fuel surcharges, a decline in other revenue, weaker trucking revenue, and reduced export coal prices offset gains in merchandise pricing and higher intermodal and coal volumes. The good thing is that FCF for the quarter was $560 million, which was just enough to cover the dividends and share buybacks. The company ended the quarter with a $130 million increase in cash and cash equivalents.

Volumes fell across Agricultural and Food Products, Minerals, Metals, and Equipment and Fertilizers y/y. Intermodal and Coal were up.

Overall, I’m very pleased with the earnings, even though the company’s earnings declined. I like the more disciplined approach to spending FCF. My target portfolio weight for the company remains unchanged at 5%.

I have to admit that I was hoping that Bank of America would fall short with this one. That’s because I have a covered call written, and the option is already in the money 🤣.

The company reported a slight decrease in total revenue, net of interest expense, which totaled $25.8 billion, a 2% decrease from the previous year. This drop was partly due to a reduction in net interest income, which fell by $0.4 billion, or 3%, primarily due to increased deposit costs despite higher asset yields and modest loan growth. The bank’s net income for the quarter stood at $6.7 billion, down 18% from $8.2 billion a year earlier. Adjusted for the FDIC special assessment, the adjusted net income was $7.2 billion.

Despite a decrease in average deposits, the segment added over 245,000 new checking accounts and witnessed significant growth in consumer investment accounts. Global Wealth & Investment Management saw record client balances nearing $4 trillion, up 13% year-over-year, driven by positive net client flows and higher market valuations.

Bank of America returned $4.4 billion to shareholders during the quarter. My target portfolio weight for the company remains unchanged at 5%.

I love an old-fashioned consumer staple. Revenue grew 1% y/y, however mainly due to price increases, not volume growth. But that’s something that’s common nowadays in the industry. Net earnings grew 11% y/y. Adjusted FCF for the quarter was $3.291 billion, which nearly covers $3.3 billion returned to shareholders.

Overall, the quarter was quite business as usual for P&G. The recent dividend increase was a nice touch too. It was their 68th consecutive increase. My target portfolio weight for the company remains unchanged at 7.5%.

Another beloved consumer staple. Global unit case volume grew 1%, revenues up 3%, and EPS grew 3%. Operating margin declined 11.8 percentage points, but the adjusted operating margin grew 0.6 percentage points. The company gained value share in total nonalcoholic ready-to-drink beverages. FCF was $158 million, an increase of $274 million versus the prior year.

The company made a significant change in the net change in operating assets and liabilities. The $2.845 billion represents the net change due to adjustments in working capital components like accounts receivable, inventories, and payables, impacting the cash flow statement for the quarter. However, the company still has a lot of cash on hand. The tax litigation with the U.S. Internal Revenue Service is still unresolved.

Nothing out of the ordinary for Coca-Cola this quarter. My target portfolio weight for the company remains unchanged at 5%.

Just like Microsoft, Visa had an awesome quarter as well. Revenue was up 10%, net income up 10% as well. Payments Volume was up 8%, Cross-Border Volume up 16%, and Processed Transactions up 11%. The company returned $8.458 billion to shareholders during the quarter.

During the quarter, Visa reached an agreement with U.S. merchants, more than 90 percent of whom are small businesses, lowering credit interchange rates and capping those rates into 2030. Visa also announced the acquisition of Pismo, a global cloud-native issuer processing and core banking platform. With the transaction complete, the combination of Visa and Pismo will provide clients with core banking and card-issuer processing capabilities across all product types via cloud-native APIs. Pismo’s platform will also enable Visa to provide support and connectivity for emerging payment schemes and RTP networks for financial institution clients.

All-in-all, it was a good quarter for Visa. My target portfolio weight for the company remains unchanged at 7.5%.

My darling oil stock. The company obviously benefited from high oil prices during the quarter. Exxon generated $14.7 billion from operations and FCF of $10.1 billion. Shareholder distributions were $6.8 billion for the quarter. The company increased its cash during the quarter by $1.7 billion to $33.349 billion.

The company reached the highest first-quarter refining throughput since the Exxon and Mobil merger in 1999. Capital and exploration expenditures were $5.8 billion, consistent with the company’s full-year guidance of $23 billion to $25 billion. Exxon also made a final investment decision on the sixth major development in Guyana. The merger with Pioneer Resources was approved at its annual meeting, and the transaction is expected to close in the second quarter of 2024.

I’m very happy with Exxon’s performance this quarter. I wish there was more room for Energy companies in my portfolio. Having said that, my target portfolio weight for the company remains unchanged at 2.5%.

Revenue was practically flat, Humira sales are still declining. However, total revenues from Neuroscience and Oncology were up this quarter.

AbbVie recently completed the acquisition of ImmunoGen. This transaction added ImmunoGen’s flagship antibody-drug conjugate (ADC), Elahere (mirvetuximab soravtansine-gynx), for folate receptor-alpha (FRα)-positive platinum-resistant ovarian cancer (PROC), to the company’s portfolio. The FDA also authorized Elahere for the treatment of FRα-positive, platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal adult cancer patients treated with up to three prior therapies. There is a lot more, but I don’t think that’s a good idea to mention it here 🤣.

I’m not that fond of these results. It seems that AbbVie can’t easily replace Humira and still loses market share across other segments of its business. Having said that, my target portfolio weight for the company remains unchanged at 2.5%, but I’ll be watching AbbVie’s results closely in the upcoming quarters.

The OG sin stock. I wasn’t sure if the disposal of ABI investment was a good idea for Altria. Of course, in the short term, it will provide them a substantial amount of cash to supplement new acquisitions and shareholder distributions. But in the long term, I don’t think that buying another e-cigarette or marijuana company will do any good. However, given recent news about reclassifying marijuana, it may breathe some life into Altria’s Cronos investment.

Revenues were down 3.6%, margins down 0.2 percentage points. Conventional smoking products units produced were down 9.9%, as well as oral tobacco products at -7.1%. The company bought back 46.5 million shares during the quarter and paid $1.7 billion in dividends. The company also retired $1.1 billion worth of long-term debt outstanding.

Even though Altria shows signs of a slowly dying company, I consider it a reliable dividend payer in the mid-term. My target portfolio weight for the company remains unchanged at 2.5%.

Products made by TI are something that I came across daily during my Uni time. Their products and shareholder approach are something that I admire. But given the headwinds in semis right now, the company is struggling.

TI saw a decrease in revenue to $3.66 billion, down 16% from $4.38 billion in the same quarter the previous year. This decline was noted across all end markets. EPS was $1.20, which included a 10-cent benefit from items not in the original guidance, down from $1.85 year-over-year, reflecting a 35% decrease. Free cash flow for the trailing twelve months was $940 million, down 79% from $4.4 billion in the prior year, impacted heavily by increased capital expenditures. TI’s total debt stood at $14.19 billion as of the end of Q1 2024, up from $10.13 billion at the end of Q1 2023.

I think that’s enough of bad news (even though there were much more). The company is obviously in a bad place right now, but I think in the long run, they will be fine. Only a dividend cut may force me to get rid of this position. My target portfolio weight for the company remains unchanged at 5%.

It was nice going over the results. Some are disappointing, some are upbeat. I excluded Unilever, Rio Tinto, Realty Income, General Mills,and Shell from this post. I plan on doing the second part after Shell releases its earnings. Thanks for reading.